Student Loan Forgiveness 2.0: Latest Updates 2026 & How to Qualify for up to $20,000 Relief

Student Loan Forgiveness 2.0: Understanding the Latest Updates for 2026 and How to Qualify for up to $20,000 Relief

The landscape of student loan debt in the United States is constantly evolving, and with each passing year, new policies and programs emerge to address the financial burden faced by millions of borrowers. As we look ahead to 2026, the discussion around student loan forgiveness 2026 is more relevant than ever. This comprehensive guide will delve into the anticipated changes, current programs, and crucial steps you can take to understand and potentially qualify for significant relief, possibly up to $20,000 or more.

For many, student loans represent a significant hurdle to achieving financial stability, delaying major life milestones such as homeownership, starting a family, or saving for retirement. Recognizing this, policymakers continue to explore various avenues for relief. The concept of student loan forgiveness 2026 is not a static one; it’s a dynamic interplay of legislative efforts, administrative actions, and ongoing economic considerations. Staying informed is your best defense against misinformation and your strongest tool for securing the relief you deserve.

This article aims to be your definitive resource, breaking down complex information into actionable insights. We’ll examine the historical context of student loan forgiveness, the current state of affairs, and what borrowers can realistically expect in the coming years, particularly focusing on the opportunities that may arise by 2026. Whether you’re a recent graduate, a long-term borrower, or someone considering higher education, understanding these updates is paramount.

The Evolving Landscape of Student Loan Forgiveness Programs

Student loan forgiveness is not a new concept. Various programs have existed for years, primarily targeting specific professions or circumstances. However, the sheer volume of student debt has prompted broader discussions and the introduction of more expansive relief initiatives. The period leading up to and including 2026 is expected to be a critical time for these discussions and potential implementations.

Understanding the current framework is essential before we project into what student loan forgiveness 2026 might entail. Currently, several federal programs offer pathways to forgiveness:

- Public Service Loan Forgiveness (PSLF): Designed for borrowers working in qualifying non-profit or government jobs. After 120 qualifying monthly payments, the remaining balance on Direct Loans may be forgiven.

- Income-Driven Repayment (IDR) Plans: These plans adjust monthly payments based on income and family size. After 20 or 25 years of payments (depending on the plan and loan type), any remaining balance may be forgiven. Recent administrative changes have significantly improved the count of qualifying payments for many borrowers under IDR plans.

- Teacher Loan Forgiveness: Offers up to $17,500 in forgiveness for eligible teachers who work for five consecutive full academic years in low-income schools.

- Total and Permanent Disability (TPD) Discharge: For borrowers who are totally and permanently disabled, their federal student loans can be discharged.

- Closed School Discharge: If your school closed while you were enrolled or shortly after you withdrew, you might be eligible to have your federal student loans discharged.

- Borrower Defense to Repayment: For students who were defrauded by their schools.

These existing programs provide a baseline, but the political and economic climate often dictates the appetite for broader initiatives. The significant administrative actions taken in recent years to streamline IDR and PSLF programs, as well as targeted forgiveness efforts, indicate a continued focus on alleviating student debt. What this means for student loan forgiveness 2026 is a potential expansion or refinement of these efforts, possibly introducing new criteria or increasing relief amounts.

Anticipating Changes: What Could 2026 Bring for Student Loan Forgiveness?

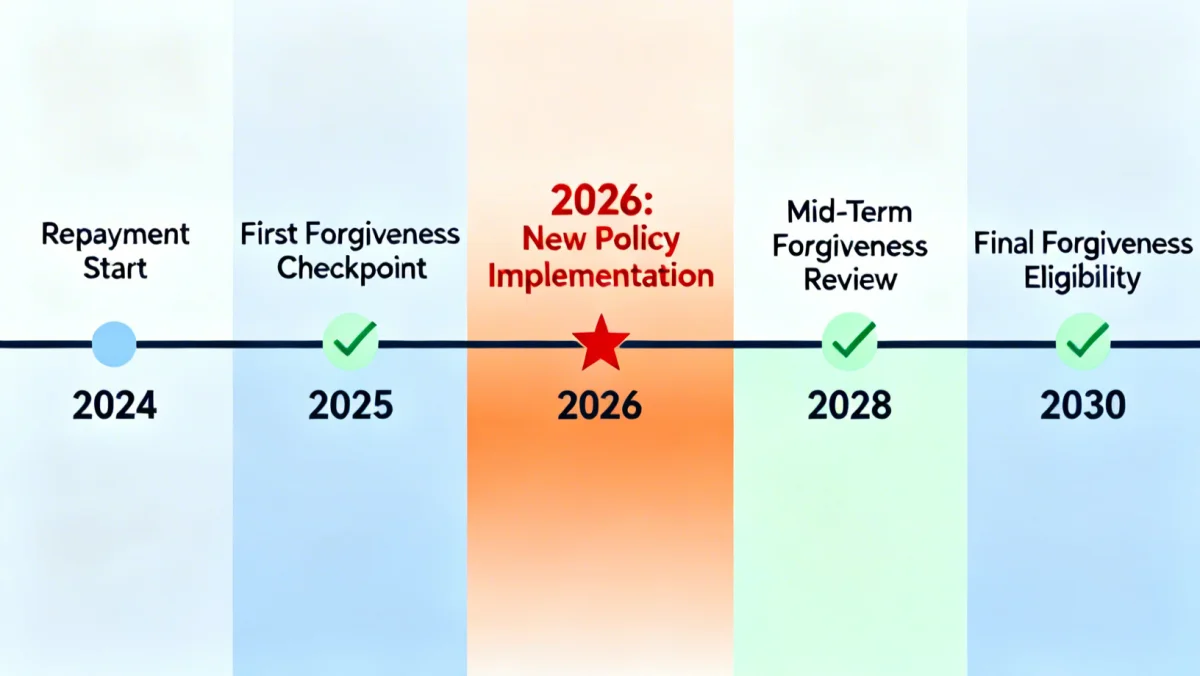

The year 2026 is not an arbitrary date; it often falls within the timeframe where new legislative cycles have matured, or administrative initiatives have had time to be developed and implemented. Predicting exact policies is challenging, but we can analyze current trends and political discussions to anticipate potential developments concerning student loan forgiveness 2026.

Potential for New Legislative Action

Historically, significant changes to student loan policy often require congressional action. While broad-based forgiveness has faced legislative hurdles, targeted programs or expansions of existing ones could gain traction. Discussions often revolve around:

- Income Thresholds: Adjusting income caps for eligibility to include more middle-income borrowers.

- Loan Type Inclusion: Expanding forgiveness to include more types of federal loans, or even a pathway for private loan relief, though the latter is less likely.

- Automatic Enrollment: Implementing systems for automatic enrollment in IDR plans or forgiveness programs for eligible borrowers, reducing administrative burdens.

- Increased Forgiveness Amounts: While $10,000 or $20,000 has been discussed, future legislation could aim for higher amounts or tie forgiveness to specific economic indicators.

Administrative Reforms and Expansions

Even without new legislation, the Department of Education has considerable power to enact changes through regulatory adjustments and administrative actions. We’ve seen this with the ‘IDR Adjustment’ (also known as the ‘Fresh Start’ initiative) that has brought millions of borrowers closer to forgiveness by correcting past administrative errors in payment counts. These types of reforms could continue to be a cornerstone of student loan forgiveness 2026, focusing on:

- Further IDR Enhancements: Ongoing efforts to simplify IDR plans, make them more affordable, and accelerate the path to forgiveness. The new SAVE Plan is a prime example of such an enhancement, significantly reducing monthly payments for many.

- PSLF Streamlining: Continued efforts to simplify the Public Service Loan Forgiveness program, making it easier for eligible public servants to navigate and receive the benefits they’ve earned.

- Targeted Relief for Specific Groups: Identifying and assisting specific populations who have been disproportionately affected by student debt, such as those who attended predatory institutions or who are in default.

The focus on equity and ease of access will likely remain central to any administrative changes concerning student loan forgiveness 2026. Borrowers should pay close attention to official announcements from the Department of Education.

Qualifying for Relief: Key Criteria and Actionable Steps

Regardless of what new policies emerge by 2026, certain foundational aspects of qualifying for student loan forgiveness are likely to remain. Proactive steps now can position you favorably for future opportunities.

Understanding Your Loan Types

The type of loan you have is often the most critical factor in determining eligibility. Federal student loans are typically the focus of forgiveness programs. Private student loans, issued by banks or private lenders, rarely qualify for federal forgiveness programs. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to become eligible for certain programs like PSLF or IDR forgiveness.

Income and Employment Requirements

Many forgiveness programs are tied to your income level or your employment sector. For IDR plans, your discretionary income directly impacts your monthly payment and the timeline to forgiveness. For PSLF, working for a qualifying government or non-profit employer is non-negotiable. Future iterations of student loan forgiveness 2026 might introduce new income thresholds or expand eligible employment categories.

Payment History and Certification

For programs like PSLF and IDR, a documented history of qualifying payments is crucial. This often requires annual certification of your income and family size for IDR, and employment certification for PSLF. Failing to certify can lead to delays or even loss of progress towards forgiveness. It’s vital to keep meticulous records of all payments and communications with your loan servicer.

Actionable Steps for Borrowers: Prepare for 2026

- Know Your Loans: Log in to StudentAid.gov to view all your federal student loans. Understand their types, balances, and interest rates.

- Consolidate if Necessary: If you have older FFEL or Perkins Loans, consider consolidating them into a Direct Consolidation Loan. This is often a prerequisite for accessing many federal forgiveness programs and could be crucial for future student loan forgiveness 2026 initiatives.

- Enroll in an IDR Plan: If you’re struggling with payments, or if your income is relatively low, enrolling in an Income-Driven Repayment plan (like SAVE, PAYE, IBR, or ICR) can significantly reduce your monthly burden and put you on a path to forgiveness.

- Certify Your Employment for PSLF: If you work in public service, make sure you are regularly certifying your employment with your loan servicer. Don’t wait until you think you’ve made 120 payments.

- Keep Meticulous Records: Document every payment, every communication with your loan servicer, and any official correspondence regarding your loans. This can be invaluable if you need to dispute payment counts or eligibility.

- Stay Informed: Regularly check official sources like StudentAid.gov, the Department of Education, and reputable financial news outlets for updates on student loan policy. Avoid scams and rely only on official information.

- Update Contact Information: Ensure your loan servicer and StudentAid.gov have your current mailing address, email, and phone number so you don’t miss critical updates or deadlines.

Understanding the ‘Up to $20,000 Relief’ Context

The figure ‘up to $20,000 relief’ often refers to specific proposals or past initiatives. For example, the Biden-Harris administration’s initial broad forgiveness plan aimed to cancel $10,000 in federal student loan debt for most borrowers and $20,000 for Pell Grant recipients. While this specific program was blocked by the Supreme Court, the amount remains a benchmark in discussions about significant relief.

When considering student loan forgiveness 2026, it’s important to understand that ‘up to $20,000’ could manifest in several ways:

- New Broad Forgiveness Initiative: A new legislative or administrative action that mirrors or adapts the previous broad forgiveness attempt, potentially with adjusted eligibility criteria or amounts that could include up to $20,000 for certain groups.

- Enhanced IDR Forgiveness: The cumulative effect of lower payments and faster forgiveness under improved IDR plans (like the SAVE Plan) could result in many borrowers having balances of $20,000 or more forgiven over time, especially those with smaller initial loan amounts.

- Targeted Forgiveness Expansion: Specific programs for teachers, healthcare workers, or other public servants could see increased forgiveness caps, potentially reaching or exceeding the $20,000 mark.

- Borrower Defense/Closed School Discharges: Victims of fraudulent schools or those impacted by school closures often receive full loan discharges, which can easily exceed $20,000. These programs are ongoing and continue to provide significant relief.

The key takeaway is that while a universal, automatic $20,000 forgiveness might not be guaranteed, various pathways exist, and more could emerge by 2026, allowing many borrowers to achieve substantial relief that could total this amount or more through a combination of programs or a single, impactful initiative.

The Role of the SAVE Plan in Future Forgiveness

The Saving on a Valuable Education (SAVE) Plan, launched in 2023, is perhaps the most significant administrative change to student loan repayment and forgiveness in recent years. It replaces the Revised Pay As You Earn (REPAYE) Plan and offers substantial benefits that will undoubtedly play a role in student loan forgiveness 2026 and beyond.

Key Benefits of the SAVE Plan:

- Lower Monthly Payments: The most significant change is the reduction of payments on undergraduate loans from 10% to 5% of discretionary income, effective July 2024. This dramatically lowers the financial burden for many borrowers.

- Interest Subsidy: For the first time, unpaid interest no longer accrues if a borrower makes their full monthly payment, even if that payment is $0. This prevents loan balances from growing, a common problem under previous IDR plans.

- Faster Path to Forgiveness for Smaller Balances: Borrowers with original principal balances of $12,000 or less can receive forgiveness after as few as 10 years of payments, with an additional year of payments required for every additional $1,000 borrowed, up to a maximum of 20 or 25 years. This accelerated timeline is a game-changer for many.

- Increased Income Exemption: The amount of income protected from discretionary income calculations has increased to 225% of the federal poverty line, meaning more income is exempt from payment calculations.

The SAVE Plan is designed to make monthly payments more affordable and to provide a clearer, faster path to forgiveness for millions. For those looking towards student loan forgiveness 2026, enrolling in the SAVE Plan (if eligible) is a critical step. Its structure means that many borrowers will see their balances steadily decrease or even be completely forgiven much sooner than under previous IDR plans, potentially leading to the ‘up to $20,000’ relief through consistent, affordable payments.

Avoiding Scams and Finding Reliable Information

Unfortunately, the promise of student loan forgiveness often attracts predatory scams. As you navigate the path to student loan forgiveness 2026, it’s crucial to be vigilant. Remember these key points:

- Official Sources Only: Always rely on information directly from the U.S. Department of Education or your official loan servicer. StudentAid.gov is the definitive resource.

- Never Pay for Forgiveness: There are no fees to apply for federal student loan forgiveness or IDR plans. Any company asking for an upfront fee to help you get forgiveness is a scam.

- Be Wary of Unsolicited Offers: Phone calls, emails, or text messages promising immediate or guaranteed forgiveness are almost always scams.

- Don’t Share Personal Information Lightly: Never give your Federal Student Aid (FSA) ID, Social Security number, or bank account information to an unsolicited caller or email.

If you have questions or suspect a scam, contact your loan servicer or the Department of Education directly through their official channels. Do not use contact information provided in suspicious communications.

The Economic and Social Impact of Student Loan Forgiveness

Beyond individual relief, the broader implications of student loan forgiveness 2026 are significant. Economists and policymakers debate the impact on inflation, consumer spending, and the overall economy. Advocates argue that reducing student debt can stimulate economic growth by freeing up disposable income for other investments, such as housing, entrepreneurship, and retirement savings.

Furthermore, forgiveness programs have a profound social impact. They can help address wealth disparities, particularly for minority groups and low-income individuals who disproportionately carry student debt. By alleviating this burden, individuals can pursue higher education more freely, leading to a more educated workforce and a more equitable society.

The ongoing discussion around student loan forgiveness 2026 is not just about financial numbers; it’s about the future of education, economic mobility, and social justice in America. As policies evolve, their impact will resonate through individual lives and the national economy.

Conclusion: Preparing for Your Future with Student Loan Forgiveness 2026

The journey through student loan repayment can be long and challenging, but the possibility of significant relief, including up to $20,000 or more, is a tangible reality for many borrowers. As we approach 2026, the landscape of student loan forgiveness continues to evolve, offering new opportunities through administrative reforms and potential legislative actions.

Your best strategy is to be proactive and informed. Understand your current loan situation, explore existing programs like PSLF and the SAVE Plan, diligently manage your payments and certifications, and stay vigilant against scams. By taking these steps, you can position yourself to take full advantage of any new or expanded student loan forgiveness 2026 initiatives. Don’t let the complexity deter you; empower yourself with knowledge and take control of your financial future.

Remember, the goal is not just to manage debt but to overcome it, allowing you to achieve your personal and professional aspirations without the crushing weight of student loans. The path to relief is clearer than ever, and with careful planning, 2026 could be a pivotal year for your financial freedom.