Navigating 2026 Student Loan Changes: Repayment Options & Forgiveness

The landscape of student loans is in constant flux, and as we approach 2026, borrowers are once again facing significant changes that could impact their financial futures. Understanding these shifts in repayment options and potential forgiveness programs is not just beneficial; it’s essential for effective financial planning. The upcoming adjustments are designed to address long-standing concerns about student debt burden, offering both new challenges and opportunities for millions of Americans. This comprehensive guide aims to shed light on what to expect in the 2026 student loan environment, helping you navigate the complexities and make informed decisions.

For years, student loan debt has been a pressing issue, affecting economic mobility and personal financial stability. The federal government, along with various advocacy groups, has been continuously working towards solutions that balance borrower relief with fiscal responsibility. The changes anticipated by 2026 are a culmination of these efforts, reflecting a move towards more flexible and potentially more forgiving repayment structures. Whether you are a current student, a recent graduate, or someone who has been managing student debt for years, these updates will undoubtedly play a crucial role in your financial strategy. Our focus here is on providing a clear, actionable understanding of the 2026 student loan changes, ensuring you are well-prepared for what lies ahead.

The Evolving Student Loan Landscape: What to Expect by 2026

The year 2026 is poised to be a pivotal moment for student loan borrowers. Several factors contribute to this evolving landscape, including legislative actions, regulatory changes, and economic considerations. The primary goal behind many of these anticipated changes is to make student loan repayment more manageable and equitable, particularly for those who are struggling financially. As we delve into the specifics, it’s important to remember that while some changes are already set in motion, others are still under discussion and may be subject to further refinement. Staying informed is your best defense against unexpected financial burdens.

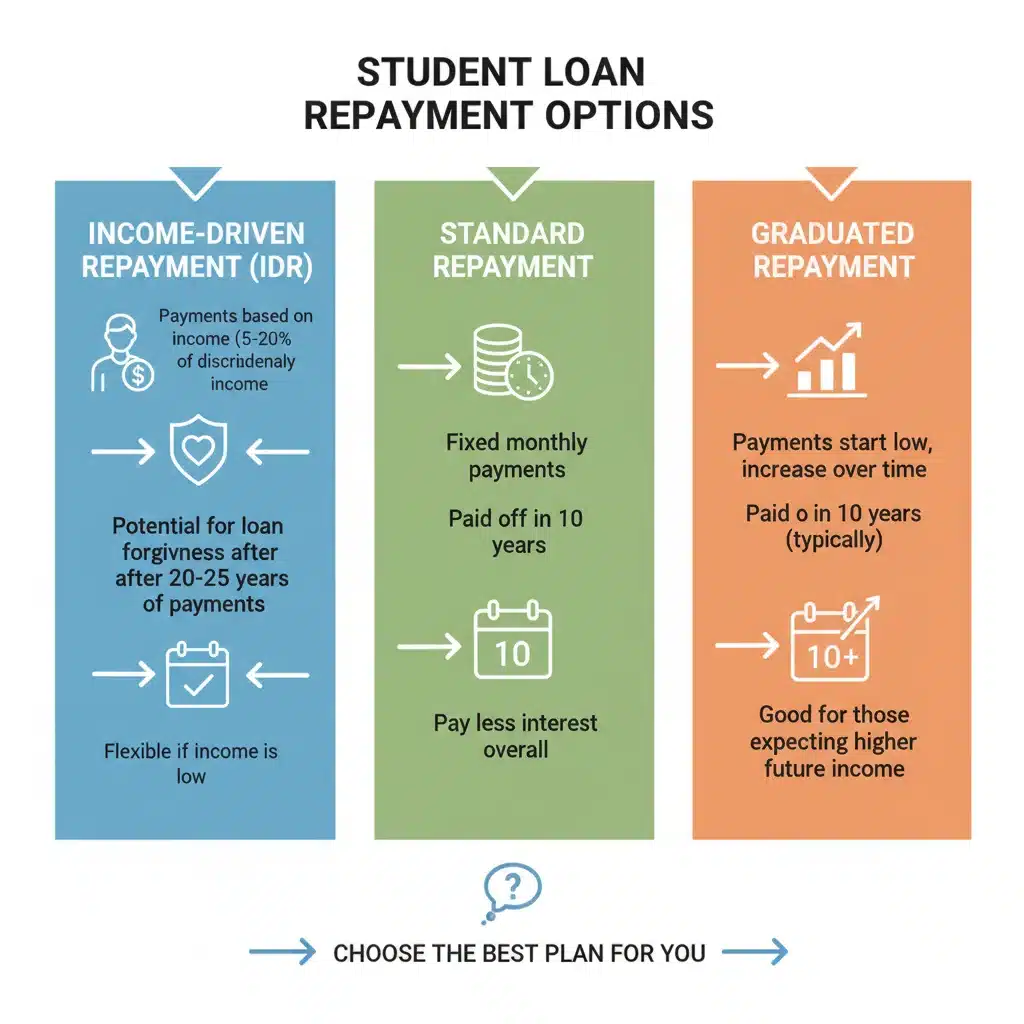

One of the most significant areas of focus for the 2026 student loan environment is the refinement and introduction of new income-driven repayment (IDR) plans. These plans are designed to cap monthly payments based on a borrower’s income and family size, offering a safety net for those with lower earnings relative to their debt. The aim is to prevent defaults and provide a clearer path to loan forgiveness after a certain period of payments. Additionally, there’s ongoing discussion about simplifying the application process for these plans, making them more accessible to borrowers who need them most. The current system, while beneficial, has often been criticized for its complexity and administrative hurdles. Simplifying it would be a major win for borrowers.

Beyond IDR plans, the conversation around student loan forgiveness continues to be a central theme. While broad-based forgiveness remains a topic of political debate, more targeted forgiveness programs are expected to be expanded or introduced. These programs often focus on specific professions, such as public service workers, teachers, and healthcare professionals, or individuals who have experienced significant financial hardship. The Public Service Loan Forgiveness (PSLF) program, for instance, has undergone reforms in recent years, and further improvements are anticipated to streamline the process and ensure more eligible borrowers receive the relief they deserve. Understanding the criteria for these programs will be crucial for anyone hoping to benefit from them.

Another area of potential change involves interest rates and loan terms. While federal student loan interest rates are typically set annually based on market conditions, there might be legislative efforts to introduce new mechanisms for capping or reducing interest accrual, especially for borrowers in financial distress. Longer repayment terms could also be explored, offering lower monthly payments but potentially increasing the total interest paid over the life of the loan. These structural adjustments aim to provide more flexibility, allowing borrowers to better align their loan payments with their financial capacity. The overarching theme for the 2026 student loan outlook is one of increased flexibility and support, but with a strong emphasis on proactive engagement from borrowers.

New Repayment Options: A Closer Look at What’s Coming

As we approach 2026, the discussion around new repayment options for student loans is gaining momentum. The goal is to create a more sustainable and less burdensome system for borrowers. The current suite of repayment plans, while offering some flexibility, has often been criticized for its complexity and for not adequately addressing the needs of all borrowers. The anticipated changes aim to rectify these issues, providing clearer, more accessible, and more effective pathways to debt management. Understanding these new options is paramount for anyone navigating student loan debt.

Streamlined Income-Driven Repayment (IDR) Plans

One of the most significant developments expected is the further streamlining and potential consolidation of Income-Driven Repayment (IDR) plans. Currently, there are several IDR plans, each with its own set of rules and eligibility criteria (e.g., PAYE, REPAYE, IBR, ICR). This complexity often leads to confusion and underutilization. By 2026, we could see a simplification into fewer, more cohesive plans, making it easier for borrowers to understand their options and enroll in the most beneficial plan for their circumstances. The new IDR plans are likely to offer more generous terms, such as a lower percentage of discretionary income used to calculate payments and a shorter path to forgiveness for some borrowers, particularly those with smaller loan balances.

The Biden administration has already taken steps in this direction with the Saving on a Valuable Education (SAVE) Plan, which significantly reduces monthly payments for many borrowers and offers interest subsidies. It’s highly probable that elements of the SAVE plan will be further integrated and expanded upon by 2026, becoming the cornerstone of the federal student loan repayment system. Key features to watch for include:

- Lower Discretionary Income Calculation: A reduction in the percentage of discretionary income used to calculate monthly payments, making payments more affordable for a wider range of borrowers.

- Interest Subsidies: Continued or expanded provisions where the government covers unpaid interest, preventing loan balances from growing even when payments are made.

- Shorter Path to Forgiveness: Forgiveness after a shorter period of payments (e.g., 10 or 20 years instead of 20 or 25 years) for certain borrowers, especially those with original loan balances under a specific threshold.

- Automatic Enrollment: Potential for automatic enrollment or easier re-enrollment processes to ensure more eligible borrowers benefit from these plans without administrative hurdles.

Expanded Access to Repayment Assistance

Beyond IDR plans, there’s a strong push to expand access to other forms of repayment assistance. This could include temporary payment pauses during periods of economic hardship, similar to the COVID-19 payment pause, but perhaps more targeted and integrated into the standard repayment framework. Furthermore, discussions are ongoing about how to better support borrowers who are nearing retirement age but still carrying student debt, potentially through specialized forbearance or deferment options that consider their unique financial situations.

Another area of innovation could be the introduction of new tools and resources to help borrowers better manage their loans. This might involve enhanced financial counseling services, more user-friendly online portals for managing loans, and clearer communication from loan servicers about available options. The goal is to empower borrowers with the knowledge and tools they need to make informed decisions and avoid default.

Potential Forgiveness Programs: What’s on the Horizon?

Student loan forgiveness remains a highly debated and impactful topic. While universal forgiveness has faced significant political and legal challenges, targeted forgiveness programs are likely to see continued expansion and refinement by 2026. These programs are often designed to address specific inequities, incentivize public service, or provide relief to borrowers facing severe financial distress. Understanding the eligibility criteria and application processes for these potential programs will be crucial for borrowers seeking relief.

Public Service Loan Forgiveness (PSLF) Enhancements

The Public Service Loan Forgiveness (PSLF) program has been a cornerstone of targeted forgiveness efforts, designed to encourage individuals to work in public service roles. Despite its noble intentions, PSLF has historically been plagued by low approval rates and complex requirements. Recent reforms have aimed to simplify the process and retroactively credit payments, bringing relief to many previously denied borrowers. By 2026, we can anticipate further enhancements to PSLF, potentially including:

- Permanent Simplification: Making the temporary waivers and flexibilities introduced in recent years permanent, ensuring a smoother path to forgiveness for future public servants.

- Broader Eligibility: Expanding the definition of ‘qualifying employment’ or ‘qualifying payments’ to include more types of public service or more payment scenarios.

- Improved Communication: Mandating clearer and more proactive communication from loan servicers to borrowers about their PSLF eligibility and progress towards forgiveness.

- Automated Tracking: Developing more robust systems for automatically tracking qualifying payments, reducing the administrative burden on borrowers.

These enhancements are critical for ensuring that PSLF fulfills its promise to public servants, making careers in essential fields more financially viable. If you are in public service or considering such a career, closely monitoring these developments is essential for your long-term financial planning regarding your student loan 2026 outlook.

Targeted Forgiveness for Specific Professions and Circumstances

- Teacher Loan Forgiveness: Existing programs for teachers in low-income schools may see increased funding or expanded eligibility criteria.

- Healthcare Professionals: Forgiveness programs for doctors, nurses, and other healthcare workers, especially those serving in underserved communities, could be expanded to address healthcare disparities.

- Borrower Defense to Repayment: This program, which provides forgiveness for students defrauded by their institutions, is likely to continue to be a focus, with efforts to streamline the application process and provide relief to more eligible borrowers.

- Total and Permanent Disability (TPD) Discharge: Enhancements to the TPD discharge process, making it easier for borrowers with disabilities to have their loans discharged, potentially through automatic data matching with other federal agencies.

- Closed School Discharge: Continued efforts to provide relief for students whose schools closed while they were enrolled or shortly after they withdrew.

These targeted programs, while not offering universal forgiveness, play a vital role in addressing specific challenges and providing relief where it is most needed. Staying informed about the eligibility requirements for each program is crucial. Many of these programs require specific types of loans (e.g., federal direct loans) and adherence to certain employment or enrollment criteria. Proactive research and engagement with your loan servicer will be key to accessing these benefits.

Strategic Planning for Your Student Loan 2026

With the anticipated changes in the 2026 student loan landscape, strategic planning is more important than ever. Proactive engagement and informed decision-making can significantly impact your financial well-being. Don’t wait for announcements; start preparing now by understanding your current situation and exploring potential future options. The goal is to optimize your repayment strategy, minimize interest, and maximize any available forgiveness opportunities.

Review Your Current Loan Portfolio

The first step in any effective strategy is to thoroughly understand your current student loan portfolio. This includes:

- Identify Loan Types: Distinguish between federal and private loans. Federal loans are typically eligible for IDR plans and forgiveness programs, while private loans generally are not.

- Understand Interest Rates: Know the interest rate for each of your loans. Higher interest rates should often be prioritized in repayment strategies.

- Check Loan Balances: Keep track of your principal and accrued interest for each loan.

- Know Your Servicer: Understand who services your loans and how to contact them. They are your primary point of contact for repayment options and information.

Access your loan information through the Federal Student Aid (FSA) website for federal loans. This portal provides a comprehensive overview of your federal loan history, current balances, and servicer details. For private loans, you’ll need to check with your individual lenders.

Evaluate Current Repayment Plan Against New Options

Once you have a clear picture of your loans, evaluate your current repayment plan. Are you on a standard 10-year plan, a graduated plan, or an income-driven repayment plan? Compare your current plan’s terms and benefits with the anticipated new options for 2026. For example, if new IDR plans offer lower discretionary income calculations or shorter paths to forgiveness, it might be advantageous to switch. Use online calculators and resources to model different scenarios based on your income and family size.

Consider the SAVE plan if you haven’t already. It offers significant benefits for many borrowers, and elements of it are likely to be central to future repayment strategies. Assess if consolidating your federal loans could be beneficial, especially if it allows you to access better repayment or forgiveness programs. However, be aware that consolidation can sometimes reset your payment count for forgiveness programs like PSLF, so proceed with caution and seek expert advice if unsure.

Stay Informed and Seek Professional Advice

The student loan landscape is dynamic, and information can change rapidly. Make it a habit to regularly check official sources, such as the Department of Education’s website and reputable financial news outlets. Sign up for email updates from your loan servicer and the FSA. Attend webinars or informational sessions offered by government agencies or non-profit organizations dedicated to student loan counseling.

For complex situations, or if you feel overwhelmed, consider seeking advice from a certified financial planner or a student loan counselor. These professionals can provide personalized guidance, help you understand the nuances of different programs, and assist you in developing a tailored strategy for your student loan 2026 planning. Be wary of scams offering quick fixes or requiring upfront fees; legitimate student loan assistance is typically free or low-cost.

Challenges and Considerations for Borrowers

While the anticipated changes in the 2026 student loan landscape offer promising avenues for relief, borrowers must also be aware of potential challenges and considerations. Navigating these complexities requires vigilance and a proactive approach. Understanding the potential pitfalls can help you avoid them and ensure you make the most informed decisions for your financial future.

Administrative Hurdles and Communication Gaps

Historically, one of the biggest challenges for student loan borrowers has been navigating the administrative processes. This includes applying for IDR plans, certifying employment for PSLF, and ensuring payments are correctly tracked. Even with anticipated simplifications, administrative hurdles can persist. Borrowers often report issues with:

- Loan Servicer Changes: Transfers between loan servicers can sometimes lead to lost documentation or payment miscounts. Keep meticulous records of all communications and payments.

- Complex Applications: While simplification is a goal, initial rollout of new programs or changes might still involve detailed application processes. Read instructions carefully and follow them precisely.

- Communication Lapses: Borrowers may not always receive timely or clear information from their servicers about new options or changes to their accounts. Actively seek out information and confirm details.

To mitigate these issues, maintain thorough records of all your loan documents, payments, and correspondence with your servicer. Consider sending important documents via certified mail to have proof of delivery. Regularly check your loan statements and the Federal Student Aid website for discrepancies.

Impact on Credit Scores and Future Borrowing

Your student loan repayment strategy can have a significant impact on your credit score. While IDR plans can make payments more affordable, consistently making payments on time is crucial for building good credit. Conversely, defaults or delinquencies can severely damage your credit score, affecting your ability to secure future loans for a home, car, or other necessities.

When considering consolidation or refinancing, understand how these actions might affect your credit. Federal loan consolidation typically doesn’t impact your credit score significantly, but refinancing with a private lender involves a hard credit inquiry, which can temporarily lower your score. Weigh the benefits of lower interest rates or different terms against the immediate impact on your credit. Always prioritize making at least the minimum payment on time to protect your credit health.

Understanding Tax Implications of Forgiveness

A critical consideration for any student loan forgiveness program is the potential tax implications. While some types of forgiveness (like PSLF) are currently tax-free at the federal level, others might be considered taxable income. For instance, forgiveness under income-driven repayment plans after 20 or 25 years of payments is currently considered taxable income by the IRS, though this has been suspended until 2025. It’s essential to understand the tax treatment of any forgiveness you receive or anticipate receiving by 2026, as this can significantly impact your financial planning.

As the 2026 student loan landscape evolves, there may be legislative efforts to change the tax treatment of certain types of forgiveness. Consult with a tax professional to understand your specific situation and plan accordingly. Ignoring potential tax liabilities could lead to an unexpected financial burden down the line.

Economic Factors and Future Policy Changes

The broader economic environment and future political landscapes can also influence student loan policies. Economic downturns might lead to calls for more borrower relief, while periods of growth could shift focus to fiscal responsibility. Changes in presidential administrations or congressional majorities can also lead to different approaches to student loan policy. While this guide provides an outlook based on current trajectories, it’s important to remain flexible and adaptable in your financial planning.

The best approach is to build a robust financial plan that can withstand potential shifts. This includes maintaining an emergency fund, minimizing other high-interest debt, and regularly reviewing your student loan strategy. The 2026 student loan environment, while promising, still requires informed and cautious navigation.

Conclusion: Preparing for Your Student Loan 2026 Journey

The journey through student loan repayment is often long and complex, but with the right information and strategic planning, it can be successfully navigated. As we look towards the 2026 student loan landscape, it’s clear that significant changes are on the horizon, offering both new opportunities and challenges for borrowers. The anticipated enhancements to income-driven repayment plans and the expansion of targeted forgiveness programs aim to provide much-needed relief and a clearer path to financial freedom for millions.

However, the onus remains on borrowers to stay informed, proactive, and engaged with their loan servicers and official government resources. Reviewing your current loan portfolio, understanding the nuances of new repayment options, and meticulously planning for potential forgiveness programs are not just recommendations; they are essential steps. Be diligent in keeping records, understanding the fine print, and seeking professional advice when needed. The administrative complexities, the impact on your credit score, and the tax implications of forgiveness are all critical factors that require careful consideration.

Ultimately, the goal is to empower you to make the best decisions for your unique financial situation. By actively preparing for the 2026 student loan changes, you can alleviate stress, minimize your debt burden, and confidently move towards a more secure financial future. This isn’t just about managing debt; it’s about reclaiming your financial independence and achieving your long-term goals. Stay informed, stay prepared, and take control of your student loan journey.